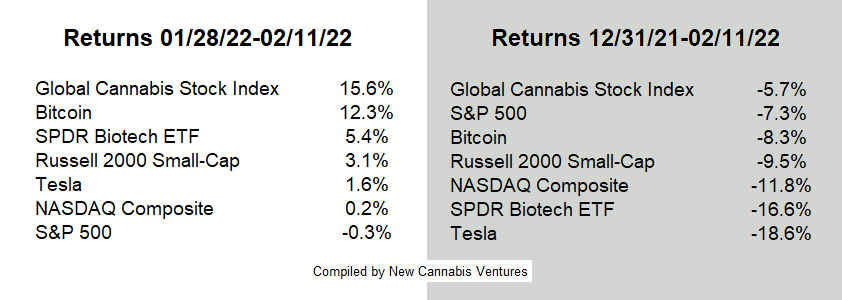

Two weeks ago, we lamented the horrible start to 2022 for cannabis stocks, pointing to the 18.4% decline in the New Cannabis Ventures Global Cannabis Stock Index during the first four weeks of the year. Since then, the index has rallied 15.6%, leaving it down 5.7% year-to-date. The improvement…

which has been supported by higher trading volumes, has far outpaced the broader stock market or other high-risk sectors that we discussed then, and the rally has resulted in cannabis stocks now being the best performers year-to-date:

Nowhere has the rebound been more evident than in the performance of American cannabis companies. The New Cannabis Ventures American Cannabis Operators Index, which currently includes 19 members (11 of which are in the Global Cannabis Stock Index), has increased by 22.6% since January 28th, a level that was the lowest closing price since October 2020. The index has now gained 6.7% year-to-date in what has been a very tough market.

The Verano acquisition of Goodness Growth has been one factor helping performance, evidenced by spectacular returns in smaller companies subsequently on hopes of more M&A, but the sub-sector of the market is enjoying broad interest over the past two weeks. Inflows into the ETF MSOS have been high. Since we detailed how the ETF has expanded so significantly three weeks ago, the number of shares has increased by almost 12%, reflecting inflows of approximately $119 million.

While the rebound by the MSOs has certainly played a key role in the improvement in the Global Cannabis Stock Index, other types of stocks have contributed as well. The New Cannabis Ventures Canadian Cannabis LP Index, now down just 1.3% year-to-date, has rallied 12% over the past two weeks. The more beleaguered New Cannabis Ventures Ancillary Cannabis Index, which is still down 12.4% year-to-date, has lifted 12.8% over the past two weeks.

If this rally holds up over the next two weeks, this would be the first monthly gain in the Global Cannabis Stock Index since last February. To say the we were due for a bounce seems like an understatement, and this may very well be only a correction of the trends that have been in place. While we think it’s a bit premature to confidently call the bottom, we are hopeful that this is the case. Three months ago, a sharp rally driven by optimism that Representative Mace’s States Reform Act would gain traction ended abruptly. This rally also seems to be partially tied to hope for federal regulatory reform, which we think will be slow to play out, but there are other factors as well, including consolidation, as discussed above, but also two fundamental changes ahead, including easier year-over-year comparisons for cannabis sales as well as the introduction of adult-use cannabis in New Jersey. We also believe that the increasing availability of debt and sale-leaseback capital is helping investors to have more confidence that future capital projects won’t require stock sales.

We are within about two weeks of the beginning of Q4 financial reports for the leading MSOs, and this will be a good…

Continue reading at NEWCANNABISVENTURES.com